When it comes to building long-term financial security, there’s one thing that consistently stands out: homeownership.

It’s not just a lifestyle choice—it’s a wealth-building strategy.

Whether you’re buying your first home, thinking about moving, or planning to sell and reinvest, understanding how homeownership affects your net worth can help you make smarter decisions. Let’s break it down.

Homeownership Is a Key to Wealth

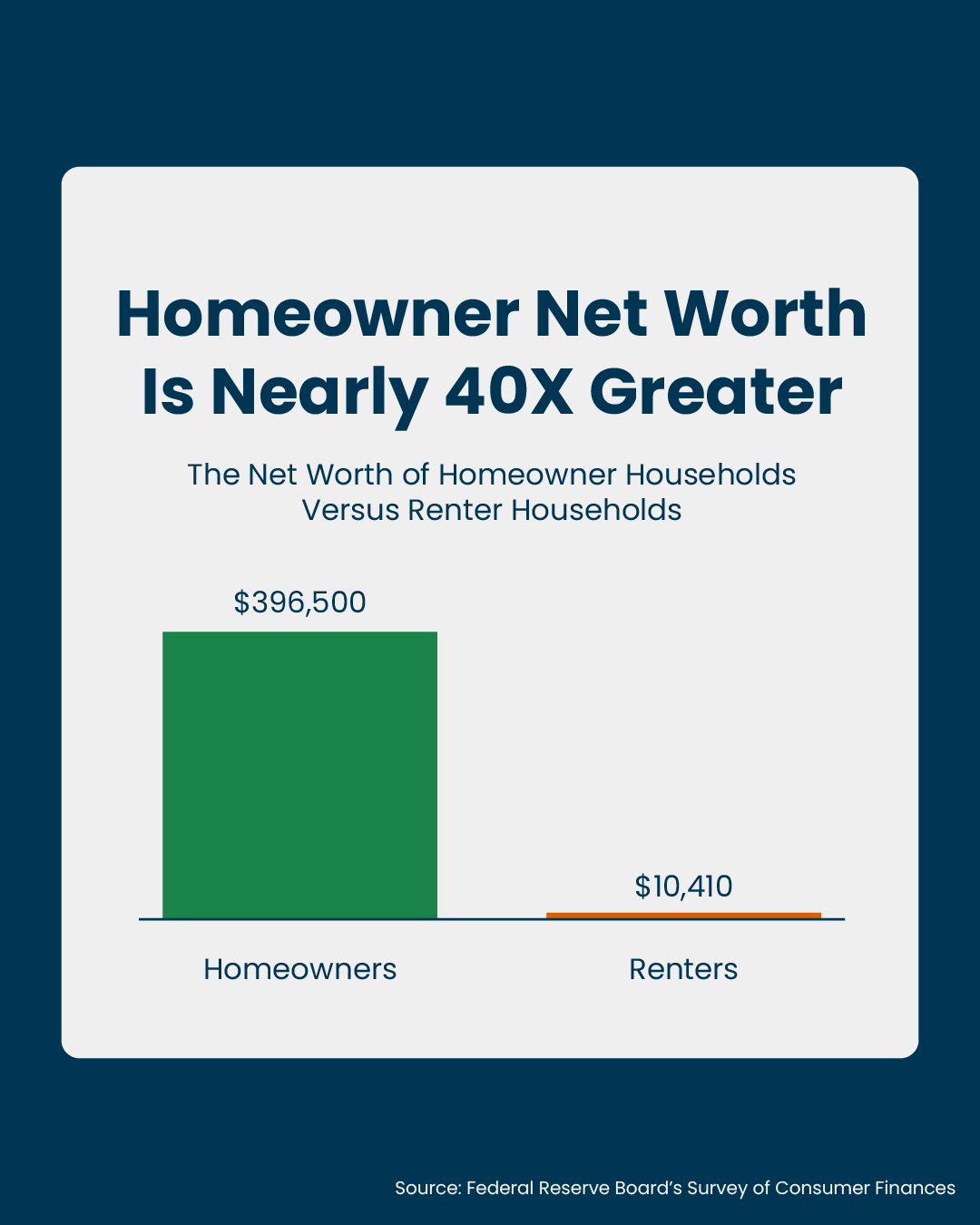

According to data from the Federal Reserve, the average homeowner’s net worth is nearly 40 times greater than that of a renter. That’s not a small gap—it’s life-changing. So why the big difference?

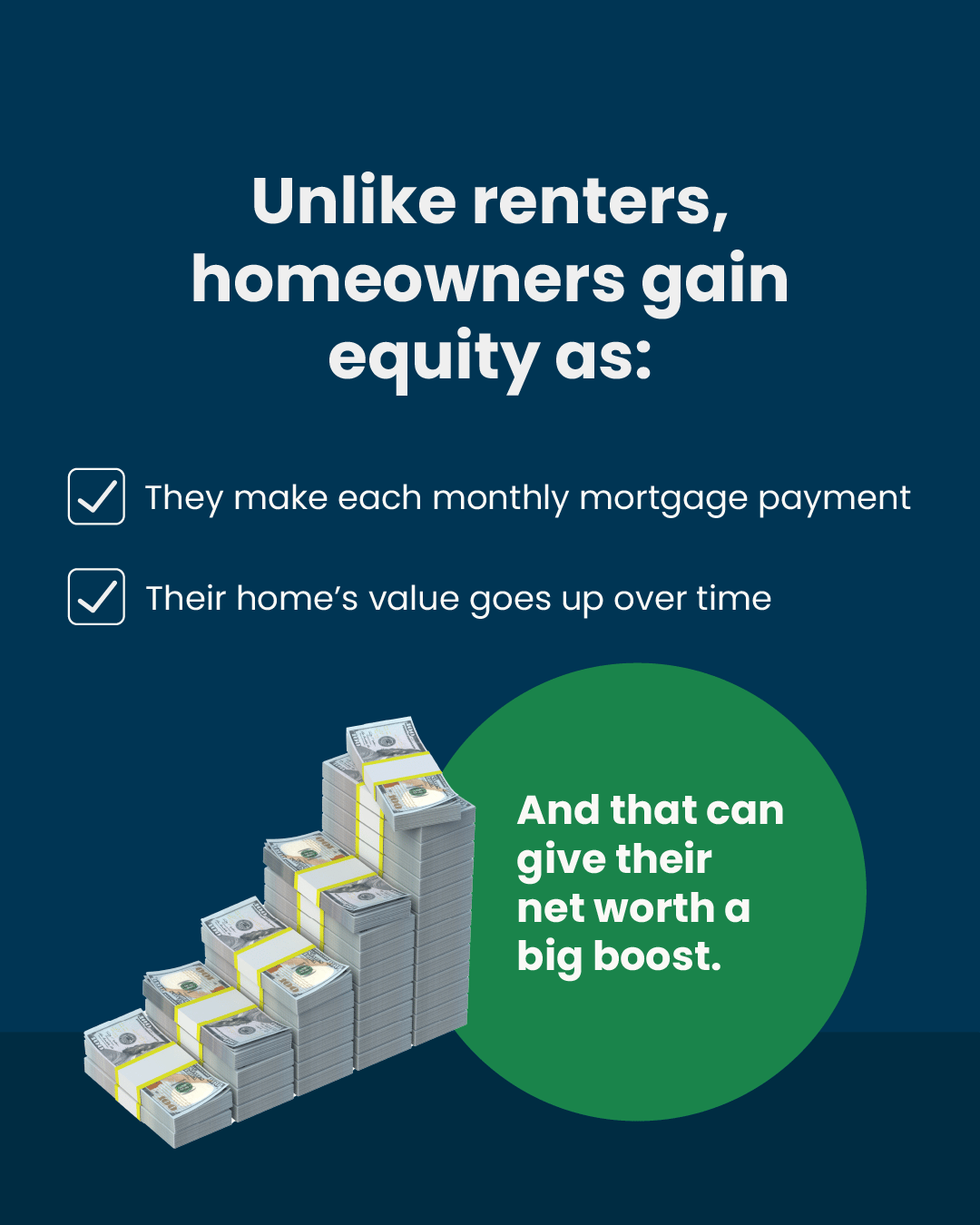

Homeowners Build Equity Over Time

-

Every time you make a mortgage payment, you’re putting money toward something you own.

-

Over time, your home’s value often increases, especially in areas with strong demand and limited inventory.

That combination—paying down the loan and appreciation—builds equity, which boosts your net worth.

This is money renters never see. Monthly rent checks go to a landlord, and once paid, that money is gone. There’s no return, no growth, and no ownership.

The Net Worth Gap Is Shocking

That’s a 38x difference in net worth. And it's not just about the home itself. Owning real estate often leads to better financial habits, more stability, and access to opportunities like home equity loans, lines of credit, or rental income.

Should You Rent or Buy?

It depends on your goals, finances, and timeline—but here’s what many people overlook: Renting may feel easier short term, but it could cost more in the long run.

The key is to think long-term. Homeownership requires upfront costs, savings, and commitment—but for those who are ready, it pays off.

Joel Berner, Senior Economist at Realtor.com, explains it well:

“Households working on their budget will find it much easier to continue to rent than to go through the expenses of homeownership. However, they need to consider the equity and generational wealth they can build up by owning a home that they can’t by renting it. In the long run, buying a home may be a better investment even if the short-run costs seem prohibitive.”

This highlights a key truth: while renting might seem like the easier option in the short term, buying offers long-term financial benefits that renting simply can’t match.

What This Means for Buyers and Sellers

For Buyers:

If you’re on the fence about buying, consider this your sign to start the conversation. Whether you’re ready now or just planning ahead, understanding how equity works can help you prepare financially and mentally.

If you’re on the fence about buying, consider this your sign to start the conversation. Whether you’re ready now or just planning ahead, understanding how equity works can help you prepare financially and mentally.

For Sellers:

If you already own a home, you’ve likely built up a substantial amount of equity. That can open the door to your next move—whether that’s upgrading, downsizing, or investing in another property. Understanding your home’s market value and your equity position is the first step.

If you already own a home, you’ve likely built up a substantial amount of equity. That can open the door to your next move—whether that’s upgrading, downsizing, or investing in another property. Understanding your home’s market value and your equity position is the first step.

The Bottom Line

Homeownership isn’t just a roof over your head—it’s a financial foundation.

If you’re ready to stop renting and start building wealth, or if you're a current homeowner planning your next step, let’s talk. We’ll map out a plan that fits your goals and timeline—whether that’s now or in the future.

Ready to explore your options? Reach out today and let’s start the conversation.

The information and opinions in this article are not investment advice. Tim Stice makes no guarantees about accuracy or completeness. Always do your own research and consult a professional before making financial decisions. Tim Stice is not liable for any loss or damage resulting from reliance on this content.

Tim Stice, Broker Realtor | Hawaii Life | Maui, Hawaii | Real Estate Agent

Tim Stice, Broker Realtor | Hawaii Life | Maui, Hawaii | Real Estate Agent