Foreclosure headlines are everywhere again. They’re designed to spark fear—and clicks. But when you dig into the actual numbers, the story looks a lot different than what you might assume from the headlines alone.

Yes, foreclosure starts are up 7% during the first half of 2025. But that doesn’t mean we’re headed toward another housing crisis. When you step back and look at the big picture, things look much more stable.

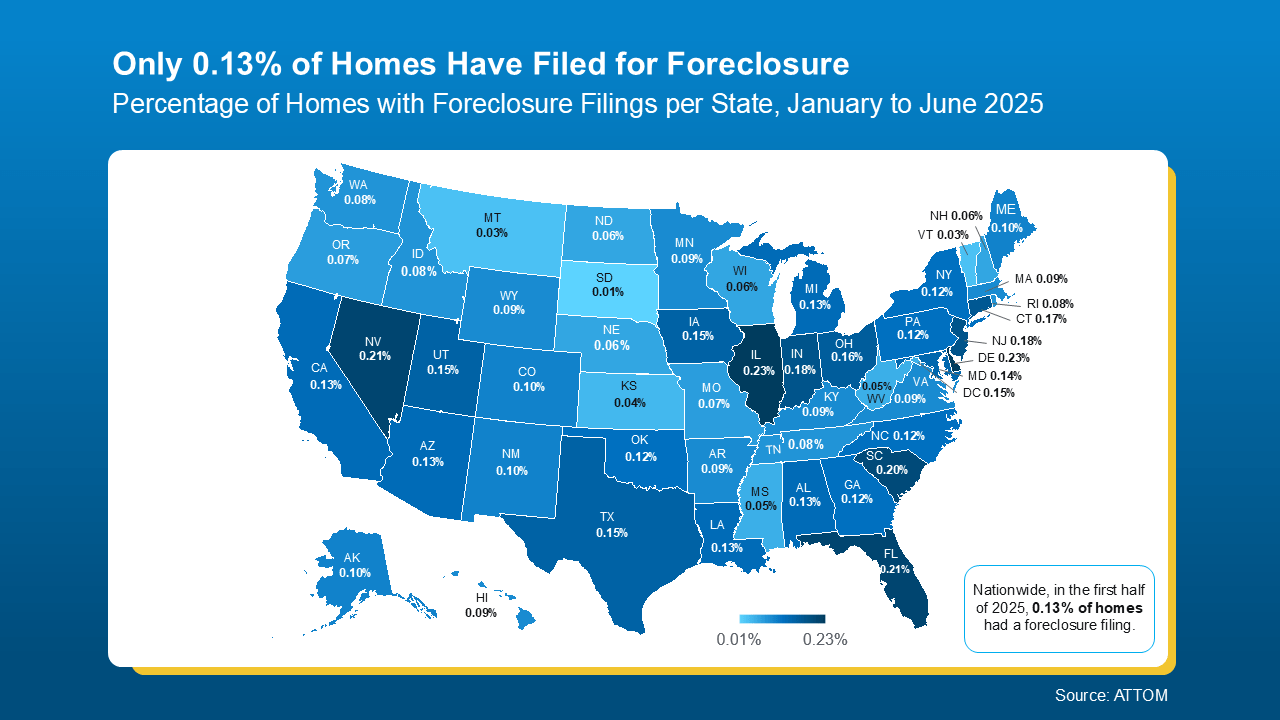

Foreclosure Filings Are Still Historically Low

Despite the recent uptick, overall foreclosure activity remains minimal. In the first half of 2025, only 0.13% of U.S. homes had a foreclosure filing. That’s less than a quarter of one percent.

To put it plainly: the overwhelming majority of homeowners are not in foreclosure. That said, real estate is always local, and foreclosure rates vary from market to market.

For context, data from ATTOM shows in the first half of 2025, 1 in every 758 homes nationwide had a foreclosure filing. That's the 0.13% you can see in the map above. But in 2010, back during the crash? Mortgage News Daily says it was 1 in every 45 homes.

No Signs of a Market Collapse

What most people remember about the last crash is the massive wave of foreclosures that hit the market all at once. That happened because of risky lending practices, adjustable-rate mortgages, and buyers with little to no equity. When home values dropped, many borrowers were underwater—and had no way out.

Today’s market looks nothing like that.

-

Lending standards are tighter

-

Homeowners have built up record levels of equity

-

Most borrowers are locked into low, fixed mortgage rates

-

If someone faces hardship, they often have the ability to sell before foreclosure becomes necessary

As Rick Sharga, Founder of CJ Patrick Company, puts it:

“. . . a significant factor contributing to today’s comparatively low levels of foreclosure activity is that homeowners—including those in foreclosure—possess an unprecedented amount of home equity.”

That equity acts as a financial cushion. Even homeowners in difficult situations often have the flexibility to sell their home, pay off the mortgage, and walk away with money in hand.

What If You’re Facing Financial Trouble?

If you’re a homeowner who’s struggling to keep up with your mortgage, you might have more options than you think. Talk to your lender early. Many banks offer forbearance, loan modifications, or can help you explore alternatives to foreclosure. The key is acting early.

Bottom Line

Foreclosure activity in 2025 is still very low by historical standards. Yes, there’s been a slight increase, but we’re nowhere near a housing crash. The market is fundamentally different from what it was in 2008—and stronger because of it.

Curious how this impacts your home’s value or your buying or selling plans? Let’s connect. I’ll help you sort through the noise and understand what the data actually says.

The information and opinions in this article are not investment advice. Tim Stice makes no guarantees about accuracy or completeness. Always do your own research and consult a professional before making financial decisions. Tim Stice is not liable for any loss or damage resulting from reliance on this content.

Tim Stice, Broker Realtor | Hawaii Life | Maui, Hawaii | Real Estate Agent

Tim Stice, Broker Realtor | Hawaii Life | Maui, Hawaii | Real Estate Agent